Is it possible to refuse to pay these fees?

Insurance coverage for citizens is a norm enshrined at the legislative level (Chapter 34 of the Tax Code of the Russian Federation and Law No. 125-FZ). The employee does not have the right to refuse them, and such an opportunity is not provided for by law.

Socially significant areas are financed from insurance funds: medicine, future pensions, benefits, maternity, and insurance payments.

Please note that insurance premiums are paid by the employer. They are calculated as a percentage of earnings (taxable income), but the contribution itself is paid at the expense of the employer.

Expert opinion

Zakharov Vasily Vladimirovich

Practicing lawyer with 6 years of experience. Specialization: family law. Legal expert. Vasily

Insurance coverage is not deducted from the employee's earnings. Consequently, even if the refusal were legalized, the amount of contributions would not increase the employee’s salary, but would only save the employer money.

The right to dispose of contribution amounts

Russian citizens do not have the right to refuse insurance coverage, but it is quite possible to manage this money independently. What's the point?

Contributions to the Pension Fund of the Russian Federation generally amount to 22%, of which 16% always goes to the formation of an insurance pension - this is the individual employee tariff. But the remaining 6% forms the funded part of the pension, which the citizen has the right to dispose of at his own discretion.

The possibilities are not endless. Russians have the right to redirect this 6% to a non-state pension fund: then only 16% will be credited to the Pension Fund, and the remaining 6% to any non-state pension fund at the request of the insured person.

You can completely abandon funded payments in favor of forming an insurance pension. Then all 22% will form the individual worker’s tariff.

IMPORTANT! The concept of “dispose of” in this case cannot be regarded as the question “can I refuse pension contributions.” This is an incorrect interpretation. You have the right to transfer the funded part of your pension to any NPF. There is no talk of refusal.

How can you refuse pension contributions in favor of a funded pension? To do this, you will need to contact the Pension Fund at the place of registration or the multifunctional center at the place of registration. You must submit the appropriate application, take your passport and SNILS with you.

Decide in advance what to do with the savings part: either choose a more profitable NPF, or transfer all funds to the insurance part. When transferring a funded pension to a non-state pension fund, it is necessary to submit a corresponding application to the NPF itself.

By law, every citizen of the Russian Federation will receive a pension after working years. But there are a number of reasons why a person would want to give up pension contributions. This article examines the question of whether it is possible to legally refuse monthly payments to the Pension Fund and how to do this.

What are pension contributions

A citizen can apply for regular pension payments from the state when his work experience ends. This is possible if he was officially employed, and his employer regularly transferred funds to the Pension Fund. The size of the superannuation pension is determined by several factors.

Among them:

- insurance experience;

- wage;

- insurance contributions to the Pension Fund from the place of work;

- individual savings.

What officials say

“We consider active longevity as a social aspect, including such areas as health, volunteering, tourism, active participation in public life,” said Deputy Head of the Ministry of Labor Alexey Vovchenko, speaking at a recent investment forum in Sochi.

He agreed with the thesis that at the age of 45 a person in the labor market experiences great risks associated with changing jobs or changing occupations. “Again, these are risks, and not a total problem, that at this age your future career ends,” the deputy minister emphasized.

“We have included in our pension reform tools to encourage later retirement,” he said. This is, in particular, an increased pension amount when applying for an insurance pension after the generally established retirement age.

The Pension Fund on its website regularly convinces pensioners that delayed retirement is beneficial for pensioners. Is it really? As they say, trust, but verify. Let's do the math.

Is it possible to refuse pension contributions and how to do it?

The legal reform that has entered into force allows Russians to form their pension in two ways:

- the employer pays the employee’s insurance premiums at his own expense;

- The citizen independently pays the funded part.

The first option provides for a direct relationship between a person’s salary without taking into account taxation. All payments are made at the expense of the enterprise. In the second option, a citizen can influence the size of his future pension.

Every citizen has the right to know that 6% of contributions go to the maintenance of state funds, and the remaining 16% participate in the formation of a pension on an individual basis. 10% consists of a fixed insurance part, and 6% - from a funded part.

The state does not give a citizen of the Russian Federation the right to refuse pension contributions, but he can shift this responsibility only to the employer.

How much of our salary do we pay as pension contributions?

Quite significant, in fact. When we believe that we give only 13% of income taxes to the state, this is a big myth. It’s better to get rid of it as quickly as possible and begin to understand how everything really works.

The fact is that formally only 13 percent tax is actually withheld from our earnings. But a huge amount of social contributions, again formally, falls on the employer.

The company you work for pays contributions for your future pension and social insurance (for example, from these insurance contributions you will be paid sick leave in case of illness or maternity benefits if we are talking about the birth of a child). Also, do not forget about contributions for “free” medicine and other specific fees (such as fees for injuries, if the work involves a risk of injury).

It is clear that the employer does not take money for these contributions out of nowhere. In fact, your organization plans such expenses as the cost of paying you.

That is, you are the one who earns from these contributions and pays for them, although according to the law it is believed that this is not the case. But when we move on to specific amounts, sometimes we really want to give up some of these deductions and ask for this money for ourselves.

So, pension contributions alone account for 22 percent of your earnings. Moreover, the total earnings, and not the one you receive in your hands. This is an even larger percentage of the amount you receive as salary. Take a third of your salary - you can't go wrong.

To refuse pension contributions even for an employee with an average salary (provided that it is “white”) is, for example, to afford to pay an average mortgage with this money.

In total, we give the state almost half of what we earn in the form of various contributions, although we often do not know about it. Formally, the employer does this for us.

So a state that supposedly receives money only from oil sales is also a big myth. The country's budget rests to a large extent on our taxes and other contributions to the treasury from the earnings of any working Russian.

Main reasons for refusal

All registered entrepreneurs are required to make insurance contributions to the Pension Fund of the Russian Federation for each hired employee. But there is a funded part, which is formed by the employee himself. Depending on the situation, the employee may qualify for a waiver of this portion.

This happens in most cases for the reason that citizens are not confident in the reliability of the PF operation.

The following reasons explain this:

- Low standard of living for pensioners in the country.

- Ambiguous relationship between insurance contributions and real pension payments after completion of work experience.

- If the state received insurance premiums for him throughout the life of an individual citizen, then in the event of his death before retirement, the money remains in the treasury and is not transferred to his heirs.

- Citizens do not have the right to withdraw funds from their own savings fund before retirement age, even for a good reason.

- Since the establishment of the Pension Fund, not a single official audit has been registered. This gives citizens reason to doubt its “transparency.”

- According to statistics, most of the funds in the Pension Fund are spent monthly on payments for 20% of the population. This indicates a significant difference in the amount of pensions for different segments of the population.

- Changes are constantly being made to the regulations for calculating insurance payments.

Algorithm and conditions of the procedure

An application for waiver of the funded part of a future benefit in favor of insurance premiums should be submitted with the following content:

- name of the body - territorial branch of the Russian Pension Fund;

- full form of the addressee (full name) or the person authorized by the power of attorney;

- personal information about the insured citizen;

- Date of preparation;

- endorsement signature.

If a future pensioner transfers powers to an authorized person, then in addition to the application and the passport of the insured citizen, a power of attorney, endorsed by a notary office, should be attached. This form must contain a complete list of actions, including the signing of such documents. For this, it is also allowed to use a single portal of State Services or Russian Post.

The refusal of the accumulative share of the benefit is unilateral, and it will be impossible to return to it after 12 months. Therefore, a citizen should weigh the negative and positive aspects of this matter. Full information about the future fate of the pension can be obtained from the Russian Pension Fund branch. If you do not withdraw the application, then all funds will be transferred to the insurance fund, and the burden of payments will fall on the shoulders of the employer.

Along with this, the population of the country has the right to independently enter into an agreement with any non-state pension fund (it is recommended to sign an agreement with organizations listed in the state register). This will allow you to create savings on your own initiative using your own investments.

The amount of contributions, timing of receipt of payment and further disposal of funds are regulated on the basis of the conditions specified in the agreement. Therefore, you should carefully familiarize yourself with the activities of a particular Non-State Pension Fund.

How not to pay

As discussed above, a person cannot refuse insurance premiums. At the same time , he can apply for payments to the Pension Fund at the expense of the employer . To do this, he needs to submit documents to waive the funded part. In this case, additional investments will no longer be able to affect the size of the future pension.

Refusal procedure

A citizen who has chosen a system of insurance contributions through a funded account must write a corresponding application to his employer and to the Pension Fund. He has the right to withdraw his application within 12 months.

Expert opinion

Zakharov Vasily Vladimirovich

Practicing lawyer with 6 years of experience. Specialization: family law. Legal expert. Vasily

The employee does not need to take any additional actions to implement his decision. Once his application is reviewed, the accumulation of pension savings will be completed automatically.

For those who have decided to abandon the savings system, the relevant question is what will happen to the savings that have already been generated up to now. The pension fund guarantees that all savings will be paid during the pension period.

The size of the future pension is determined by several parts, including the funded one. A citizen of the Russian Federation has the right to refuse the funded component in favor of a fixed insurance component. As a result, the accumulation part will cease to form.

Having abandoned the funded pension, it will no longer be possible to return to it after one year. Therefore, the applicant should carefully consider their decision before submitting documents. One of the advantages of the funded system is, in the event of the death of a citizen, the possibility of transferring unpaid insurance benefits to the relatives of the deceased.

Every citizen has the right to receive advice from a Pension Fund employee on any issues related to insurance premiums.

To begin the procedure, the employee must contact his employer with a corresponding application. Before submitting an application to waive a funded pension, it is worth familiarizing yourself with the main stages of the procedure. This will allow the issue to be quickly resolved in favor of the applicant.

Next, the person will have to go to the nearest PF branch. The application will be formed from the following aspects:

- name of the Pension Fund;

- Full name of the citizen or authorized representative;

- purpose of the application (refusal of accumulative contributions in favor of fixed insurance);

- date, signature.

After studying the details of the case, the applicant's employer will continue to pay 22% for the employee in the PF. The funds received will be distributed as follows:

- 16% for the formation of an insurance pension;

- 6% for the maintenance of state funds and current fixed payments.

Reference. In the Russian Federation, private non-state pension funds officially exist. Any Russian, at his own discretion, can apply to such an organization to form a funded pension. The size and frequency of contributions, as well as the right to dispose of the accumulated capital, are strictly specified in the agreement between the parties.

This article examines the following questions: how a pension is calculated in the Russian Federation, why a person might want to refuse insurance contributions and how to do this.

A Russian has the right to abandon the funded system in favor of a fixed insurance pension . As a result, the size of the pension will depend on the actual salary. In this case, all deductions will be made by the enterprise at its own expense. This is the only legal way to avoid insurance deductions.

The procedure for accumulating pensions

Insurance premiums, the amount of which depends on the amount of wages, are calculated as a percentage of the monthly salary without deducting taxes.

The higher the salary, the greater the contributions and, accordingly, the greater the retirement pension. Additional Information! In accordance with the requirements of the law, the tariff rate for contributions to the Pension Fund of the Russian Federation today is 22%. Regardless of the direction chosen by the employee, the distribution of withheld funds occurs as follows:

- 16% falls on the personal account of the insured person. This is his IT (individual tariff);

- the remaining 6% is called the solidarity tariff. These are funds intended to finance social benefits, in particular burial and other fixed payments.

If the employee has chosen only the insurance direction, all 16% will be used to complete the insurance coverage.

If contributions are directed to accumulation, the distribution of funds will be carried out as follows:

- 10% — insurance premium;

- 6% - accumulation.

The main sources of filling the storage part include:

- 6% of the IT of the insured employee, deposited into the account of the Pension Fund of the Russian Federation by the employer.

- Voluntary contributions of individuals made within the framework of the State Co-financing Program.

- Maternal capital. Only women can send funds.

- Investments.

Advantages and disadvantages of directions

Before making a final decision, it is necessary to become more familiar with the pros and cons of each direction. The table below will help you decide whether you should give up saving your pension or not.

| Insurance direction | Cumulative direction | |

| Advantages |

|

|

| Flaws |

|

Attention! The moratorium on the formation of a funded pension was extended until 2020, that is, all 16% of the insured employee’s IT is directed to the formation of insurance coverage.

Useful video

The video has even more information on the topic:

It is impossible to completely abandon a pension, because the right to receive a pension benefit is assigned to every citizen at the legislative level. After the 2020 reform, two types of pensions appeared: funded and insurance.

Under some circumstances, you can refuse the savings account, but obtaining insurance coverage is mandatory. So is it possible to refuse a pension in Russia? You will find the answer to this question below.

Termination of pension payments

The right to receive a pension is automatically canceled in the following cases:

- if employees of the Pension Fund discover information that is sufficient to terminate payments;

- a disabled person received the payment, but the medical certificate expired;

- the payment was made in the event of the loss of a breadwinner, but the person who received it was declared incapacitated or he had reached the borderline age;

- if a citizen officially refuses to receive the insurance part of the pension payment.

How to refuse a pension

The procedure for registering a voluntary refusal to receive pension payments depends on whether the citizen receives a pension or is entitled to receive it, but has not yet applied to the Pension Fund of Russia.

In the first case, it is necessary to submit an application to the Pension Fund at the place of residence of the pensioner; the period of refusal cannot be longer than 10 years. In the second, you don’t have to contact the Pension Fund at all; citizens automatically enjoy the right to increase the coefficient.

Voluntary renunciation of old-age pension payments

To temporarily suspend receiving an old-age pension, you must contact the Pension Fund at your place of residence with a document confirming your identity, and then:

- Fill out the application form in free form and submit the necessary documents;

- specify for what period of time you want to suspend payments - the maximum is 10 years;

- You will receive a response from the Pension Fund within 14 days.

If you change your mind, you can restore the payment of money at any time; you just need to write an application for the return of pension payments.

Is it possible to refuse to transfer money to the Pension Fund?

It is not possible to refuse to transfer funds from your salary to the Pension Fund. But you can refuse the funded part of your pension. Any employer transfers 22% of employees’ salaries to the Pension Fund.

At the same time, 16% is always transferred to the insurance part of the pension, this cannot be refused or changed, and 6%, which at the request of the citizen goes to the savings or insurance part. Any employee has the right to write a refusal to transfer this 6%. This refusal must be submitted to the Pension Fund.

Expert opinion

Zakharov Vasily Vladimirovich

Practicing lawyer with 6 years of experience. Specialization: family law. Legal expert. Vasily

In this case, the citizen will be able to receive payment of all the money from the funded part of the pension or transfer it to the insurance part, which will allow increasing the size of the pension benefit in the future.

There are also cases when payments are suspended without the request of the recipient. This may be the case in such cases.

- Loss of the right to receive payments.

- Death of a pensioner.

- When a citizen does not receive payments.

In the third case, if the pensioner does not collect the pension benefit at the post office within six months, it is suspended. The payment will be resumed after the pensioner applies to the Russian Pension Fund.

Voluntary refusal to receive a pension for a certain period allows citizens of the Russian Federation to increase its size in subsequent years. The procedure and conditions for voluntary refusal are enshrined in Federal Law No. 400-FZ “On Insurance Pensions” of December 28, 2013.

What do these directions provide?

Before abandoning the funded part of a pension in Russia, it is advisable to consider the individual advantages and disadvantages of such areas. This will allow you to form a complete picture and make the right decision.

The insurance pension allows you to:

- formulate your future pension level depending on the size of your existing salary;

- do not pay your own funds to transfer to the pension fund (here the employer pays for everything);

- index the amount of insurance contributions annually.

A funded pension allows you to:

- after reaching retirement age, receive the entire amount of previously accumulated savings in one payment;

- transfer the accumulated pension by inheritance;

- independently determine the amount of transfers to the pension fund.

Among the negative aspects of the insurance pension, it is worth highlighting the inability to return any amount of contributions if the death of a citizen occurred before the appointment of pension payments. Regarding the funded pension, it is not indexed by the state, and the increase in the amount depends solely on the employee’s personal transfers.

Voluntary refusal to receive a pension

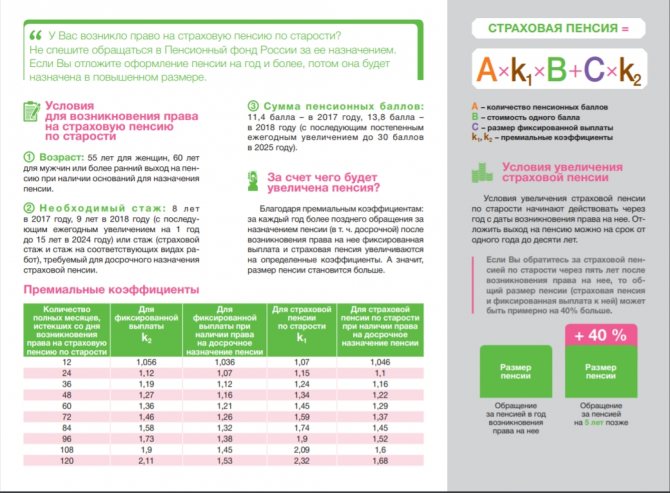

At its core, voluntary retirement is a choice of a convenient and at the same time profitable retirement. Since for each year after reaching retirement age, the pension amount will increase by a certain factor.

Who has the right to issue a voluntary renunciation of a pension?

Voluntary renunciation of a pension in accordance with current legislation can be issued by the following categories of recipients:

- persons who have already been assigned and paid an insurance pension;

- persons whose pension has not yet been assigned, upon acquisition of the right to payment.

After the expiration of the voluntary refusal period, the pensioner will be accrued and paid a pension, increased by the increase factor of the fixed fee. The size of this coefficient depends on the following three indicators:

- number of months of deferment;

- type of pension (insurance/social/in connection with the death of the breadwinner);

- procedure for retirement (by term or early).

Below is a gradation of increase coefficients for voluntary refusal to pay a pension.

| Number of months of deferment | Old age insurance pension | Early age insurance pension | Old age insurance pension in connection with the death of the breadwinner | Early age insurance pension in connection with the death of the breadwinner |

| 12 | 1,056 | 1,036 | 1,07 | 1,046 |

| 24 | 1,12 | 1,07 | 1,15 | 1,1 |

| 36 | 1,19 | 1,12 | 1,24 | 1,16 |

| 48 | 1,27 | 1,16 | 1,34 | 1,22 |

| 60 | 1,36 | 1,21 | 1,45 | 1,29 |

| 72 | 1,46 | 1,26 | 1,59 | 1,37 |

| 84 | 1,58 | 1,32 | 1,74 | 1,45 |

| 96 | 1,73 | 1,38 | 1,9 | 1,52 |

| 108 | 1,9 | 1,45 | 2,09 | 1,6 |

| 120 | 2,11 | 1,53 | 2,32 | 1,68 |

It must be remembered that to determine the increasing coefficient, only full calendar years are taken into account.

How to register a voluntary refusal to receive a pension

The procedure for refusing a pension depends on whether the citizen is a current recipient of a pension, or whether he acquired the right to payment, but did not apply for a pension.

To terminate payments to current pension recipients, it is necessary to submit an application in the established form, and you must have an identification document of the applicant with you.

The application is submitted to the Pension Fund of the Russian Federation at the place of registration of the pensioner.

The termination of payment occurs on the first day of the month following the month the pensioner submitted the application. The maximum period for which the payment of a pension is suspended, according to a voluntary refusal, is 10 years.

Citizens who acquired the right to a pension, but did not apply to the Pension Fund within the prescribed period, can take advantage of the right to automatically apply an increasing coefficient.

Expert opinion

Zakharov Vasily Vladimirovich

Practicing lawyer with 6 years of experience. Specialization: family law. Legal expert. Vasily

Let's look at an example . In March 2020, Petrov turned 60 years old. As of 04/01/18, Petrov’s length of service and IPC meet the requirements necessary for the assignment of an old-age insurance pension.

Petrov applied for a pension in March 2020, a year after acquiring the right to payment. Petrov’s pension was calculated taking into account the increasing coefficient for the fixed payment - 1.056.

Restoration of insurance pension payment

Reinstatement of the insurance pension payment is made in the following cases:

- expression of the pensioner’s wishes;

- expiration of the period specified in the application;

- expiration of the 10 year deadline.

In order to restore the pension payment at the request of the pensioner, it is necessary to go through the following procedure.

Stage 1. The pensioner must submit an application to the authorities that calculate and pay the pension and identification documents of the pensioner. Also, the Pension Fund authorities may require additional documents.

Stage 2. The Pension Fund considers the pensioner’s application within five working days from the date of receipt of this application or from the date of receipt of additionally requested documents from other authorities.

Stage 3. The pension itself is paid directly from the first day of the month following the month the application was accepted.

Let's look at an example. Pensioner Evdokimov has received a pension since February 2014. Evdokimov decided to voluntarily refuse to pay his pension.

December 11, 2020 he appealed to the Pension Fund authorities with an application for voluntary refusal to pay a pension for 3 years.

From January 1, 2020 Evdokimov's pension payment has been stopped.

Evdokimov expressed a desire to receive pension payments. He submitted a pension application dated February 05, 2020.

In March 2020, Evdokimov’s pension should be restored and paid.

When calculating the pension amount, the increase factor will only be taken into account for the full two years (24 months) - 1.12.

Suspension of pension payments

Payment of a pension can be suspended not only on a voluntary basis. Suspension of the accrual and payment of pensions may occur in the following situations:

- loss of the right to a pension;

- non-receipt of pension payments by a pensioner;

- death of a pensioner.

The pensioner can restore the payment of the pension by eliminating the circumstances that led to the suspension of the pension.

Loss of the right to a pension by the recipient

A pensioner may lose the right to a pension depending on the conditions for granting a pension, as well as due to the occurrence of a certain situation

Let's look at some of them:

Situation 1. Termination of payment of a disability pension: removal of the disability group that was previously assigned to the pensioner after undergoing re-examination (confirmation) or the pensioner’s failure to appear for re-examination.

Situation 2. Termination of payment of a survivor's pension: after the pension recipient is recognized as able to work. The pension recipient has reached the age of 18 and has not provided the Pension Fund with documents confirming that the person is studying full-time.

Situation 3. Termination of pension payment after checking the accuracy of the documents provided: as a result of checking all the documents provided, it was established that these documents were fake, and the fact that the pensioner provided false information was revealed.

Situation 4. Termination of payments due to the pensioner moving to a permanent place of residence in a foreign country.

Payment of pensions is suspended based on the order of the Pension Fund. During the period of suspension, Pension Fund employees find out the reasons why the necessary documents were not provided and carry out work to request these documents from the pensioner himself.

Non-receipt of payments

The very fact that a pensioner has not received a pension is grounds for suspending future pension payments.

The procedure for suspending pension payments consists of several stages:

Stage 1. The pensioner did not show up to receive the pension, or the postman could not deliver the pension for six months, since the pensioner did not live at the specified address.

Stage 2. After six months of non-receipt of pension funds, from the 1st day of the month, the Pension Fund temporarily suspends pension payments. The pension fund is obliged to send a notice to the pensioner.

Stage 3. If, after six months from the moment of temporary suspension of pension payment, the pensioner has not applied to the Pension Fund, then the pension payment is completely suspended and a notification is sent.

Death of a pensioner

The death of a pensioner is the main factor in the termination of pension payments.

After death, the territorial branch of the registry office submits a death certificate to the Pension Fund. The death certificate is the main document for terminating the accrual and payment of a pension. In fact, the termination of payments occurs automatically, so the relatives of the pensioner do not need to contact the relevant structures.

Expert opinion

Zakharov Vasily Vladimirovich

Practicing lawyer with 6 years of experience. Specialization: family law. Legal expert. Vasily

Payment is suspended if the pensioner is declared missing or deceased; the payment of the pension is terminated. The basis is a court decision.

Pension payment termination period:

- the next month following the date of death of the pensioner indicated in the certificate;

- from the 1st day of the month following the month the court decision was made if the pensioner is considered missing.

After the death of a pensioner, relatives, as well as legal representatives, have the right to receive pension payments from the deceased.

Any citizen of Russia who is officially employed has the right to claim a legal pension after retirement, which is formed through pension contributions from the employer.

p, blockquote 1,0,0,0,0 —>

Some of us are ready to give up this right for a variety of reasons - from doubts about the reliability of the Pension Fund to doubts about our own ability to live until retirement.

p, blockquote 2,0,0,0,0 —>

p, blockquote 3,0,1,0,0 —>

Is it possible

It is impossible to completely refuse a pension. Obtaining security is the responsibility of the Russian.

Moreover, citizens are required to pay contributions to the budget, part of which is taken from pensions. It is impossible to refuse to participate in social insurance voluntarily, but you can postpone this moment or reduce the amount of payments.

The law provides for cases when the accrual of pensions is terminated or suspended. There are 2 main reasons:

- The pensioner was declared missing or dead. The pension will cease to be received on the 1st day of the month following the date of death of the person.

- Payments are suspended for 6 months if a person intentionally does not receive it (for example, does not show up at the Post Office). If the pension is not renewed after six months, payments will be stopped until the application is submitted.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

8 (800) 700 95 53

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

The right to a pension automatically terminates when the following grounds occur:

- Pension Fund employees discovered data that is sufficient to cancel pension accruals;

- the pensioner was disabled and the medical certificate had expired;

- the citizen received a survivor's pension, but was declared incompetent or reached a certain age;

- if the relatives of the deceased who were caring for his elderly parents or children lost their pension, but became officially employed and began to receive a salary;

- the citizen applied to the Pension Fund with an application for voluntary renunciation of the insurance part of the pension (other types will continue to be paid).

Contributions to the Pension Fund are mandatory for everyone

Is it possible to refuse to pay contributions to the Pension Fund? The answer to this question is “no” if you are officially employed and do not receive a “black” salary, because these contributions are paid not by you, but by your employer, who is obliged to report to the Pension Fund of the Russian Federation so as not to cause serious trouble.

p, blockquote 4,0,0,0,0 —>

The exception is when employees are employed under an employment contract . In this case, the employer pays only income tax of 13%.

But in such a situation, its employees face many risks associated with the inability to claim other insurance payments (disability pension, maternity capital), the inability to receive paid sick leave, and so on.

p, blockquote 5,0,0,0,0 —>

The only thing a citizen can do is to choose a pension insurance system with or without a funded component. When choosing a system with a funded component, a citizen submits appropriate applications to his employer and the Pension Fund.

p, blockquote 7,0,0,0,0 —>

After receiving a positive answer, he has the right to invest his funded pension funds in the pension market, and he can win or lose. But such a system also has advantages - in particular, in the event of a citizen’s death, his relatives will be able to inherit the unpaid insurance benefit.

p, blockquote 8,0,0,0,0 —>

Taxes and contributions from salary

Personal income tax is the only type of tax withholding made directly from an employee's wages. But in addition to personal income tax, insurance contributions (for pensions, sick leave, etc.) are also charged on earnings.

Insurance coverage for workers is a legal norm that all Russian employers are required to comply with. If an organization, individual entrepreneur or individual uses the services of hired workers, then it is necessary to insure the workers and pay premiums for them.

The direct responsibilities of the policyholder (employer) are to timely and fully calculate and pay insurance premiums from the wages of employees. Moreover, the type of insurance depends on the nature of the relationship:

| Type of insurance premium | Purpose | Contribution amount (% of earnings) | Employment contract | Civil contract (author's order, contract, subcontract) |

| Compulsory pension insurance OPS | Directed towards the formation of an insurance (and funded) old-age pension upon reaching the established retirement age | Up to 22%. | It is required to be charged. Exception No. 1. We allow a transition to lower tariffs. Exception No. 2. The tariff must be reduced to 10% if the employee’s income exceeds the approved limit. In 2020, the OPS limit is 1,115,000 rubles. | |

| Compulsory medical insurance | It is used to finance healthcare institutions to provide free medical care to Russians. | Up to 5.1%. | It is required to be charged. There are no exceptions. Reduced premium rates may apply. | |

| Temporary disability and maternity insurance VNiM | It is used to pay benefits for temporary disability, child care, pregnancy and childbirth, care for the illness of close relatives, benefits for the birth of children, etc. | Up to 2.9%. | It is required to be charged. The policyholder may apply reduced rates if specified conditions are met. If the employee’s income during the reporting period exceeded the approved limit, the rate is reduced to 0%. The 2020 VNiM limit is 865,000 rubles. | Not credited. |

| Insurance against accidents and occupational diseases at work NS and PP | It is used to pay benefits for temporary disability as a result of industrial injuries, as well as one-time insurance payments for accidents and occupational diseases. | From 0.2 to 8.5%. | Always accrued. The amount of deductions is determined depending on the main type of activity of the company, the risk class and the danger of production. | At the employer's discretion. May be included in the terms of the GPC agreement. |

Sashka Bukashka's salary is 30,000 rubles.

Personal income tax 13% = 30,000 × 13% = 3900 rubles.

Salary to be issued (in hand) = 30,000 - 13% (3900) = 26,100 rubles.

Insurance premiums (OPS + compulsory medical insurance + VNIM + NS and PZ) = 30,000 × 38.5% (22% + 5.1% + 2.9% + 8.5%) = 11,550 rubles.