Nowadays, people are trying to participate in the financial activities of the country. One of the ways of such participation, the main purpose of which is to generate income, is investing.

There are various types of investment activities, but there is one that every citizen of Russia commits, although it is quite possible that he is not even aware of it.

This type of investment is the accumulation of a pension for oneself based on deductions from wages. It would seem that everyone is thinking about future security from the very first year of work, but at the same time they do not know that they are investing in their pension.

And yes, indeed, with this type of accumulation, funds “work” - they generate income, which is also deposited into your personal account.

How pension savings are formed

All pension savings located in a special part of a citizen’s individual personal account must be invested. Moreover, this applies to all funds located and transferred to the citizen’s account in the form of compulsory insurance contributions from the employer, additional contributions from the citizen himself, voluntary contributions from the employer, and state co-financing contributions. It is also possible to use maternity capital funds to form a funded pension. These funds will also take part in the investment.

If a citizen has not made a decision on the formation of a funded pension, then pension savings formed before January 1, 2014 (before the introduction of a moratorium on funded pensions) will continue to be invested. In any case, if a citizen has any pension savings, they are definitely invested.

Citizens themselves can choose the ways in which pension savings will be formed and invested. These methods can be:

- formation of pension savings, including funded pensions, through the Pension Fund of Russia (PFR);

- formation of pension savings, including funded pensions, through the Non-State Pension Fund (NPF). In this case, you can transfer the funded part of your pension to the NPF.

Important Feature

: if your employer pays mandatory insurance contributions for you, and you have voluntary pension savings, then the same investment procedure will apply to all your savings.

Let's look at these methods in more detail.

Pension system reforms

The new pension reform began in 2002. The changes adopted in it affected the transformation of an important state system from a distribution system to a management-savings system, where contributions made to the general pension fund became not impersonal, but personalized.

The new system implied the division of the pension into 3 components:

- Basic, which provided the state to each citizen with the established minimum.

- Insurance, the basis of which was monthly transfers from the salary by the employer of the percentage established by law.

- Cumulative, consisting of real money provided for investment in investment funds for profit.

Formation of a future pension

Participants in this reform were to include the male population born in 1953 and later, and women born in 1958 and younger. Then, starting from 2005, the list of applicants for funded payments was reduced. These now include only persons whose year of birth began in 1967. At the same time, citizens older than this year also have savings accounts, which they managed to form over 2 years of contributions, when the enterprise transferred 2% of the amount of their earnings to the Pension Fund. Today, upon retirement, persons who participated in the formation of a savings account for only 2 years can apply to receive a one-time payment of all the money from this account.

Since 2009, an additional co-financing program was announced, under which every citizen could voluntarily make contributions, thereby increasing their funded portion of future pension payments.

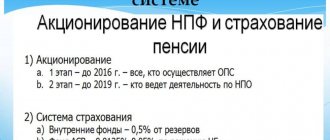

Formation of savings in the Pension Fund and Non-State Pension Funds

In 2010, the next pension reform was revised again and the number of pension components was reduced to two. This model is still in effect today:

- the insurance part accounts for 16% of deductions;

- the funded share is 6% of insurance fees.

Since 2004, citizens younger than 1967 have had to express their opinion on the direction of investment of funds held in their personalized accounts. The decision concerned which company or non-state pension fund should transfer 6% of the contributions paid monthly by the employer. In silence, they remained in the Pension Fund, whose level of profitability is slightly lower than in non-state funds.

Since 2014, everyone who had not decided to transfer their funded part to a non-state pension fund was automatically included in the model in which all 22% went to the insurance part of pension payments. At the same time, a so-called “freeze” occurred, according to which all the money contributed by the employer was transferred only to the formation of the insurance part of the pension, and in fact began to be used to pay off pension payments to current citizens who had reached the established age for a well-deserved rest. At the same time, that part of the funds that was transferred to the management of the NPF before this period remained in their accounts and continues to work, increasing the citizen’s savings account annually. True, the number of such citizens is measured only at 20%, and in the short period before the “freezing”, not so much money had accumulated in the NPF.

Classification of pension funds of the Russian Federation

Formation and investment of pension savings through the Pension Fund of Russia

If you form your pension savings through the Pension Fund, then the territorial body of the Pension Fund at your place of residence will establish and pay the funded pension.

To form a funded pension (pension savings) through the Pension Fund, you need to select one of the following investment portfolios:

a) investment portfolio of the management company (MC)

;

b) the basic investment portfolio of the state management company (GMC)

;

c) expanded investment portfolio of the State Management Company

.

The basic investment portfolio includes government securities of the Russian Federation and corporate bonds of Russian issuers. The expanded investment portfolio includes, in addition to those indicated, mortgage securities, bank deposits in rubles and foreign currencies, and bonds of international financial organizations.

Currently, the only GUK is Vnesheconombank.

The list of management companies is posted on the Pension Fund website.

Investment of pension savings will be made taking into account your choice.

You can update your investment portfolio and/or choose a different management company no more than once a year.

So, the choice of investment portfolio has been made. What's next?

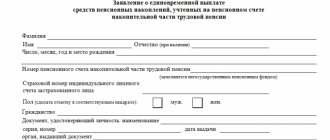

Complete an application for choosing an investment portfolio (IP) and send it to the Pension Fund.

The application can be submitted in person or sent in another way (including in the form of an electronic document or through a multifunctional center for the provision of state and municipal services).

Establishing your identity and verifying your signature when applying through a multifunctional center is carried out by the center itself.

When sending an application by mail, the signature on the application is certified by a notary.

If you personally contact the territorial office of the Pension Fund of the Russian Federation at your place of residence, you will need a passport and an insurance certificate of compulsory pension insurance.

The application deadline is no later than December 31 of the current year.

The Pension Fund considers the application by March 1 of the year following the year in which the application was submitted, and notifies you of the results of consideration of the application by March 31.

There is no need to take any action to select the expanded investment portfolio of the State Management Company. Those. if you remain silent (do not submit an application), then pension savings will automatically be invested in the expanded investment portfolio of the State Management Company.

The profitability of management companies turns out to be higher than that of non-state pension funds

Citizens born after 1967 can change the manager for the funded part of their pension once a year. Millions of Russians annually transfer their savings to non-state pension funds, forgetting about the possibility of transfer to management companies (MCs). But the direct transfer of funds to management companies allows you to avoid the costs of operating private non-state pension funds and thereby increase the profitability from investing pension savings.

Vasily Sinyaev

Lost in translation

In the spring, the Bank of Russia presented the results of managing pension savings transferred to non-state pension funds (NPFs). According to the regulator, the weighted average return on their investment exceeded inflation (2.5%) and at the end of 2020 averaged 4.6% before the payment of fees to the management company, specialized depository and fund. After the payment of remunerations, the weighted average yield decreased to 3.8%.

At the end of last year, the volume of pension savings in non-state pension funds increased by 14.3%, to 2.44 trillion rubles. The transition campaign in the compulsory pension insurance system had a significant impact on the increase in the volume of funds managed by NPFs. According to the Russian Pension Fund, following the results of the 2020 transition campaign, out of 12 million applications for the transfer of the funded part of the pension, positive decisions were made on 6.5 million applications. Moreover, 4.7 million people transferred their savings from the Pension Fund to the Non-State Pension Fund, 1.7 million people changed the Non-State Pension Fund, and 79 thousand people returned from the Pension Fund to the Pension Fund.

In addition to NPFs, citizens can transfer their pension savings to a management company. However, there are almost 1 thousand times fewer such transfers. At the end of 2020, only 9.1 thousand people changed their choice of management company, at the end of 2020 - only 4.9 thousand people. The total number of citizens using the services of management companies is also small - 430 thousand people. According to the director of strategic development of Alfa Capital, Vadim Loginov, a design feature of the accumulative element of the mandatory pension system was that the insured person, by choosing a non-state pension fund, becomes its client directly, but the choice of a management company means that his savings go there impersonally from the Pension Fund of Russia . “The managers of these people cannot offer them their services, products, etc. Future pensioners who place savings in the management company, accordingly, can count on receiving information about their investments only independently unilaterally or through government services,” notes Mr. Loginov.

Private investors needlessly underestimate the opportunity they have, because the performance of management companies is higher than that of non-state pension funds. According to the Bank of Russia, only one non-state pension fund showed a double-digit increase in profitability at the end of 2020 (minus remuneration to the management company, special depository and fund), while among managers almost two dozen companies were able to achieve such a result. TKB InvestSolid Management provided the highest income to clients; based on the results of pension savings management, the growth was 13.5% and 13.2%, respectively.

This superiority is primarily due to the current legislation, according to which NPFs cannot independently place pension savings. Investment of these funds occurs through the management company. “When deciding to transfer your pension savings to a non-state pension fund, you need to understand that in the end the pension savings will be managed through the management company,” notes Andrey Lobanov, director of the investment management department of the Management Company Region Asset Management. According to him, the main advantage of transferring pension savings directly to the management company is that the name of the company to which you entrust your savings is known in advance.

Profitability of investing pension savings of NPFs in 2017

| 11,16 | |

| "Hephaestus" | 9,97 |

| National Pension Fund | 9,81 |

| "Aquilon" | 9,71 |

| "Volga-Capital" | 9,66 |

| "Gazfond pension | 9,53 |

| savings" | |

| "UMMC-Perspective" | 9,19 |

| "VTB Pension Fund" | 9,02 |

| "Society" | 8,93 |

| "Alliance" | 8,83 |

| NPF "Surgutneftegas" | 8,74 |

| NPF Sberbank | 8,70 |

| Defense Industrial Fund | 8,62 |

| them. V.V. Livanova | |

| "Professional" | 8,59 |

| "Trust" (Orenburg) | 8,49 |

According to the Central Bank

Conservative growth

In 2020, the majority of management companies surveyed by Dengi placed an emphasis on conservative instruments - bonds, while the share of shares was minimal at the beginning of the period. “From the point of view of the relationship between potential profitability and risk, bonds looked preferable to shares, so the share of shares was zero or minimal,” says Vladimir Potapov, chairman of the board of directors. According to the general director of the Trinfico Management Company Dmitry Blagov, investments in shares were not significant due to the high risks of such an instrument in the current economic situation in Russia.

The managers' caution was justified: last year was extremely unsuccessful for the Russian stock market. At the end of 2017, the Moscow Exchange index decreased by more than 5%. At the same time, the market conditions for the bond market last year were very favorable: lower inflation and measures by the Bank of Russia to ease monetary policy. Over the past year, the Central Bank carried out five reductions in the key rate by a total of 2.75 percentage points (pp), and in the autumn months alone it was reduced twice by a total of 0.75 pp, to 7.75% - the minimum values from July 2014 (7%). “By placing primarily in high-quality bonds, management companies received an increase in coupon yield, effectively managing duration (the increase in bond prices, balancing coupon rates in the face of declining rates),” notes Dmitry Blagov. At the same time, many companies preferred OFZ. “Government securities are the most liquid bonds and react faster than other debt instruments to changes in the monetary policy of the Central Bank,” notes Andrey Lobanov.

The performance of management companies was positively impacted by the gradual disposal of long-term deposits opened at low rates in 2013-2014. The presence of such deposits froze for a long period of time funds that could have been placed in more profitable instruments after a sharp increase in rates at the end of 2014. “Only as such deposits were repaid, funds could be invested again at higher rates,” notes Andrey Lobanov.

Profitability of investing pension savings by management companies

"TKB InvestSolid Management"

| Name | Briefcase | For 2020 (% per annum) | For 2015-2017 (% per annum) |

| — | 13,16 | 12,66 | |

| "Uralsib" | — | 12,92 | 14,59 |

| "Analytical Center" | — | 12,72 | 16,72 |

| "VTB Capital Asset Management" | — | 12,13 | 15,54 |

| "VTB Capital Pension Reserve" | — | 11,90 | 14,71 |

| "Ingosstrakh-Investments" | — | 11,63 | 12,56 |

| "Trinfico" | long-term growth | 11,59 | 11,20 |

| "Leader" | — | 11,32 | 13,94 |

| "Metallinvesttrust" | — | 11,29 | 13,09 |

| "Sberbank Asset Management" | — | 11,27 | 13,47 |

| National management company | — | 11,19 | 11,00 |

| BPA | — | 11,12 | 11,05 |

| VEB | government securities | 11,09 | 12,85 |

| "Alfa Capital" | — | 10,95 | 14,50 |

According to the Central Bank.

Demand for risk

In 2020, the preferences of companies managing pension savings of citizens have changed slightly: the share of bonds dominates, but the demand for shares is growing. This is due to the limited potential for growth in bond prices against the backdrop of record low inflation and the Central Bank’s plan to further reduce rates. According to the forecasts of analysts surveyed by Dengi, they expect one or two more rate cuts this year, respectively, to 7% or 6.75%. A more aggressive rate cut will be hampered by rising geopolitical tensions between the US and Russia, as well as a global rise in base rates. According to analysts, the convergence of the differential in rates between the ruble and dollar zones has led to an increase in market volatility and the required risk premium. Region Asset Management considers the potential for further reductions in rates to be limited, so they reconsidered the risk in debt portfolios and shifted the emphasis towards liquid bonds with low duration.

Managers' interest in stocks is also growing. “This year, we continue to adhere to the idea that the stock market retains the potential for further growth, despite periodically arising difficulties in the form of various kinds of sanctions,” notes Andrey Lobanov. Managers are attracted to Russian stocks by potentially high dividend yields. Currently, the dividend yield of the Russian stock market is one of the highest compared to other emerging markets. According to Bloomberg, the dividend yield of the Moscow Exchange index is approaching 5%. According to the NRK-R.O.S.T. group, since 2014, the volume of dividends paid by companies to shareholders has increased 1.5 times and by the end of 2020 may reach 1.5 trillion rubles. “From the point of view of the potential return/risk ratio, we see the emergence of attractive investment objects on the stock market. For a number of companies, the dividend yield on shares is comparable and even exceeded the yield on traditional debt instruments, such as bonds or deposits,” notes Vladimir Potapov.

Need to know

If you change the manager of your pension savings early (if your money has been in the Pension Fund or Non-State Pension Fund for less than five years), you lose investment income.

RUB 55 billion

Lost at the end of last year were citizens who decided to change pension savings managers. At the same time, only the “silent ones” who decided to move from the Pension Fund to the Non-State Pension Fund lost 39 billion rubles.

If, while remaining in the Pension Fund, you entrust pension funds to a private management company, you will have to pay for its work.

If the insured person chooses an investment portfolio (management company, management company), the pension insurer remains the Pension Fund. The Pension Fund transfers savings to the selected management company under a trust management agreement, reserving the maintenance of personal accounts and the payment of future pensions. And it is the Pension Fund of Russia that bears the full range of responsibility for investment results, and its resources are incomparably greater than those of private non-state pension funds. General Director of Management Company "Trinfico" Dmitry Blagov reminds that the Pension Fund does not withdraw 15% of investment income to conduct its activities, as NPFs do.

When you transfer to a NPF (from the Pension Fund of the Russian Federation or another NPF), you will pay for its work, including the services of the agent who lured you away and the management company hired by the fund.

When an account is transferred to a non-state pension fund, ownership of pension savings passes to the fund, the fund determines the investment strategy, selects management companies, and in the future pays pensions. The insured person, when transferring pension funds to a non-state pension fund, does not have the opportunity to choose an investment strategy.

When investing through any market participant, your savings may rise or fall in value.

Formation of a funded pension through a non-state pension fund

You can refuse to form a funded pension (pension savings) through the Pension Fund and choose a non-state pension fund. But then the NPF will assign and pay you a funded pension. He will also invest pension savings. You can also transfer your funded pension to a non-state pension fund.

NFP works with certain management companies and manages your funds according to the right of operational management.

If you choose an NFP, you need to submit an application to the Pension Fund and then enter into an agreement with the selected NFP. There is no need to conclude an agreement with the management company.

You will conduct all further communications regarding the formation of pension savings and their investment, as well as the payment of funded pensions, with the NFP.

How to transfer from NPF to Pension Fund

Questions about how to transfer from a non-state pension fund back to the Pension Fund, as well as how to transfer from one non-state pension fund to another, often arise among citizens.

You can change the previously selected method of forming a funded pension (pension savings). Those. You can:

- transfer from the NPF to the Pension Fund (and thus return the funded part of the pension to the Pension Fund);

- transfer from the Pension Fund to the Non-State Pension Fund;

- move from one NPF to another;

- replace the investment portfolio.

To do this, you need to submit an application to the territorial office of the Pension Fund in person or send it in another way, for example, in the form of an electronic document or through the MFC.

If you have access to your personal account on the Pension Fund website, then almost all of this can be done using electronic services.

NPF or Pension Fund: what to choose

Most of you have already decided on your choice of savings method. It remains for me to give a few recommendations in relation to the current state of the pension system. But first, let’s compare the Pension Fund and the Non-State Pension Fund according to two main criteria:

Profitability

At the end of 2020, which is considered extremely profitable for the Russian stock market, the profitability of non-state pension funds averaged about 11%. VEB's average return on its portfolio of government securities and its expanded investment portfolio was 10.53% in the same year. In the 1st half of 2020, VEB’s profitability dropped to 8.8% per annum. 20 out of 66 non-state pension funds show investment results below VEB, but continue to outperform the industry average. The gap between the profitability of Pension Funds and Non-State Pension Funds is narrowing and there is now no global difference in this indicator. Due to low inflation in 2017-2018, both private and public pension funds will most likely be able to outpace it.

Risks

From the point of view of government guarantees, the Pension Fund looks like a less risky investment. On the other hand, starting from 2020, NPFs have the opportunity to join the system of guaranteeing the rights of insured persons, an analogue of the DIA. 38 NPFs are members of the Deposit Insurance Agency. But, in the event of bankruptcy, a private pension fund may lose its accreditation. The accumulated funds will be reimbursed from insurance payments and transferred to the Pension Fund. At the same time, one cannot ignore factors that undermine citizens’ trust in the state:

- freezing of the accumulative part, which has lasted for 4 years;

- lack of transparency in reforming the pension system;

- transferring the accounting of savings in the Pension Fund from cash to points.

In the case when the funded part is added to the insurance part as a result of freezing, we are not talking about investing in principle. Savings are indexed in accordance with the inflation rate only virtually. Outwardly, this looks better than the possible losses of NPFs, especially during periods of economic recession. Opponents of the savings system (for example, Deputy Prime Minister Olga Golodets) talk about the risks of bankruptcy of non-state pension funds. However, in conditions when the government changes the principles of formation of pension savings almost every year, the risks of remaining “silent” are hardly less. What's particularly troubling is that today no one can say how much the points accumulated in the account will be worth when you retire.

Arguments in favor of a non-state pension fund

- The further it goes, the more it becomes obvious that the financial model of the Pension Fund of Russia is gradually becoming obsolete. The state has less and less money; indexing does not cover the depreciation of pensions.

- The constantly changing rules for accounting for pension contributions in the Pension Fund present new surprises.

- In conditions of economic growth, which will sooner or later resume, the profitability of non-state pension funds exceeds inflation and exceeds the indicators of the Pension Fund. But over the 10-year horizon, private funds are still ahead of the state Pension Fund in terms of accumulated returns: NPF – from 80 to 100%; VEB Management Company – from 50% for the basic portfolio (government securities) to 80% for the expanded portfolio.

I also recommend reading:

What is stagflation and what does it mean?

Is the beginning of stagflation possible in Russia?!

Another argument in favor of NPFs is the promised implementation in 2019 of the idea of individual pension capital (IPC). Let me remind you that it provides for a transition from compulsory pension insurance (MPI) to a voluntary system. Now the reform to create the IPK, which I wrote about six months ago, has been postponed indefinitely. But there is a high probability that the growing pension fund deficit will force a return to this idea.

Weaknesses of NPFs

- The risk of bankruptcy of non-state pension funds, especially small private funds.

- The profitability of some non-state pension funds is losing to inflation. The main reason for the losses was investments in securities of Otkritie and B&N Bank.

- Transferring from one NPF to another earlier than 5 years leads to the loss of accrued investment income. By the way, in 2020, about 2 million citizens exchanged one fund for another. Their losses amounted to 33 billion rubles.

The main reason for the departure of former “silent people” to non-state pension funds is a total distrust of the state pension system. Of course, the activity of agents who attract clients plays a role. But neither persuasion nor deception can achieve such results. People in general do not trust private structures. But they rely even less on the state. Just think about freezing the funded pension and transferring money in personal accounts to a point system. The rules of the game change almost every year, which creates grounds for justified fears. There is no point in counting on the fact that the state will finally carry out the pension reform “as it should” and that you will receive decent payments before you retire. Salvation for most of us is in one thing: wisely and effectively invest part of your current income. The sooner you start doing this, the better.